2026 // Week 12 – Vietnam Pepper Market Update: Stability Amid Harvest Pressure

Price Outlook: Constrained Downside, Speculative Support

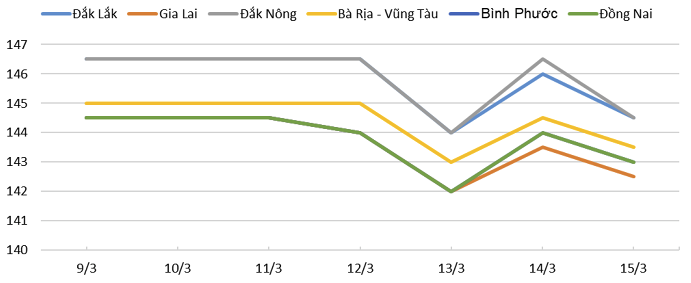

Pepper prices today maintained stability following yesterday’s widespread decline, as market participants navigate the complex interplay of harvest season dynamics, geopolitical tensions, and shifting trade patterns. Domestic Vietnamese pepper prices currently fluctuate within the range of 142,000–144,000 VND/kg, reflecting a market at a crossroads between supply expansion and persistent demand fundamentals.

Price trends of pepper in the Central Highlands and Southeast regions during the week from 09-March to 15-March.

Market Psychology

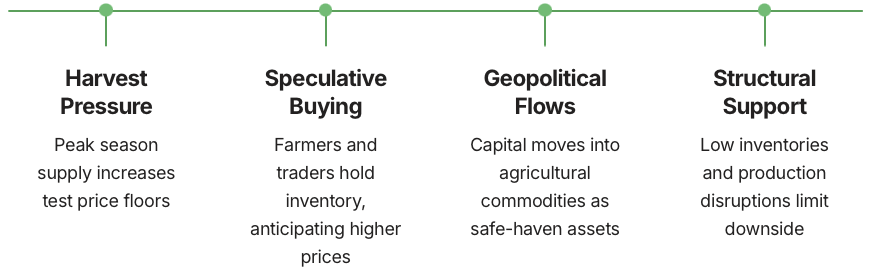

Market experts anticipate that pepper prices will face downward adjustment pressure as Vietnam enters peak harvest season, yet the magnitude of declines appears constrained by multiple countervailing forces. Traditional seasonal patterns suggest price weakness during harvest as physical supply floods markets, but structural factors—low global inventories, speculative positioning, and geopolitical risk premiums—create asymmetric downside protection that prevents sustained bearish momentum.

The expectation of higher future prices encourages inventory holding among both producers and trading houses, creating artificial supply tightness that supports near-term valuations. This speculative positioning manifests most clearly in forward curve structures, where deferred contract months trade at progressively wider premiums to spot prices, reflecting market consensus around supply constraints materializing in subsequent quarters.

Global geopolitical uncertainties indirectly benefit pepper markets through capital allocation patterns. Agricultural commodities with sufficient liquidity—like pepper, which trades on multiple exchanges and has established derivatives markets—receive disproportionate investor attention during risk-off environments. This relationship means Middle East tensions, while creating trade cost pressures, simultaneously drive speculative long positions that buoy prices. The net effect proves counterintuitive: traditional analysis would predict bearishness from harvest pressure, yet geopolitical risk premiums and speculative positioning create floor conditions that prevent sharp declines.

Looking ahead, market participants should anticipate range-bound trading with elevated volatility around key catalysts. Thailand’s sustained import demand provides structural support, while Vietnam’s harvest timing creates tactical selling pressure. Indonesia’s low inventory levels mean any supply disruption triggers immediate price spikes. The convergence of these factors suggests a market where prices fluctuate within defined bands—sharp moves occur on news events, yet sustained trends prove difficult to establish. Traders should position for mean-reversion patterns rather than directional breakouts, with particular attention to inventory data releases and geopolitical developments that shift risk sentiment.

Market Dynamics: The Dual Pressure Points

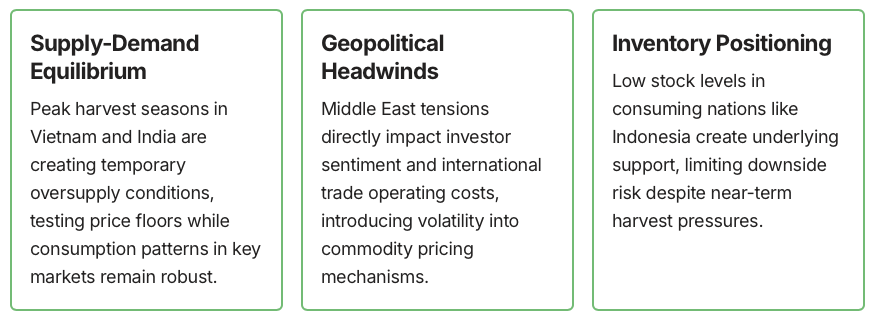

The global pepper market faces a paradoxical situation where traditional supply-demand fundamentals suggest price weakness, yet structural factors provide unexpected resilience. Geopolitical uncertainties in the Middle East are creating risk-off sentiment among commodity investors, simultaneously driving capital flows into agricultural commodities perceived as safe-haven assets. This counterintuitive relationship means that while Vietnam’s harvest season typically brings price declines, geopolitical tensions paradoxically support prices through speculative positioning in liquid agricultural markets like pepper.

Market analysts note that the downside trajectory appears capped by multiple converging factors. First, speculative stockpiling emerges when prices reach attractive levels, particularly among trading houses anticipating future supply constraints. Second, consuming countries maintain historically low inventory levels, creating a buffer against sharp price corrections. Third, the concentration of production among a few suppliers—Vietnam, Indonesia, India, and Brazil—means that disruptions in any single region ripple through the entire market, limiting sustained bearish momentum.

Thailand’s Import Surge: A Strategic Shift

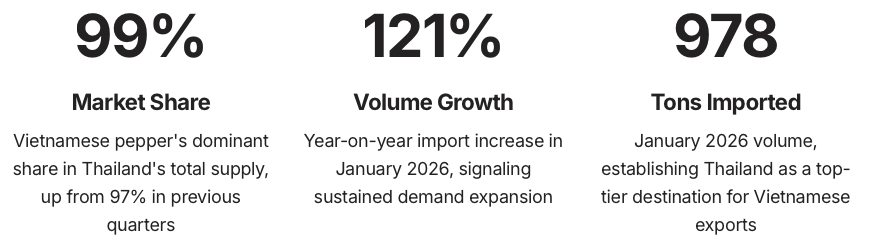

One of the most striking developments in recent pepper trade data reveals Thailand’s transformation into a major Vietnamese pepper importer. According to the Import-Export Department of Vietnam, Thailand imported 978 tons of pepper in January 2026 alone, representing a dramatic 121.2% increase compared to the same period last year. This surge is not merely a statistical anomaly but reflects fundamental shifts in Thailand’s spice procurement strategy and Vietnam’s competitive positioning.

The drivers behind Thailand’s import surge are multifaceted and interconnected. Thailand’s food processing sector continues its expansion trajectory, with pepper-intensive products ranging from ready-to-eat meals to packaged seasonings driving raw material demand. The tourism industry’s recovery creates secondary demand through restaurant and hospitality channels, amplifying consumption patterns. Critically, Thailand’s domestic pepper production remains constrained by limited suitable growing regions and aging cultivation infrastructure, forcing import dependency despite efforts at self-sufficiency.

Vietnam’s competitive advantages extend beyond mere proximity. Vietnamese pepper offers superior quality-to-price ratios compared to alternatives from India or Brazil, with consistent sizing and pungency profiles preferred by Thai processors. Established trading relationships and streamlined logistics corridors minimize transaction costs and delivery lead times. As global pepper production shows signs of decline due to climate disruptions, Thailand’s strategy of building strategic inventories through Vietnamese imports becomes increasingly rational, suggesting this trend will persist through 2026.

Production Challenges: Climate Disruptions Reshape Supply

The current harvest season presents a complex picture where traditional supply expectations collide with climate-driven production shocks. Vietnam’s key growing regions accelerated harvesting activities after the Lunar New Year holiday, with farmers attempting to maximize output before monsoon conditions intensify. However, industry sources confirm that prolonged late-season rains during critical flowering and fruiting periods last year have already reduced yield potential, with initial estimates suggesting 10-15% output declines compared to normal seasons.

India’s situation proves even more severe, with disease outbreaks following natural disasters significantly reducing productivity across major pepper-growing states. Kerala and Karnataka, historically accounting for 70% of India’s pepper production, report widespread vine mortality and reduced berry formation. Unlike Vietnam’s weather-related temporary setbacks, India’s disease challenges may persist into subsequent seasons, requiring vine replacement cycles that stretch 2-3 years before full productivity returns. This structural constraint differentiates India’s situation from Vietnam’s cyclical weather impacts.

Indonesia and Brazil, while maintaining steady production, lack the scale to materially alter global supply balances. Indonesia focuses primarily on domestic consumption and traditional markets, with export capacity constrained by infrastructure limitations. Brazil’s pepper industry remains relatively small and fragmented, unable to absorb demand shifts from disrupted Asian supplies. The net effect: new crop supply pressure exists but is insufficient to drive sustained bearish momentum, particularly as speculative buying provides near-term price support.