2026 // Week 18 – Global Pepper Market Update : Market Structure & Intelligence

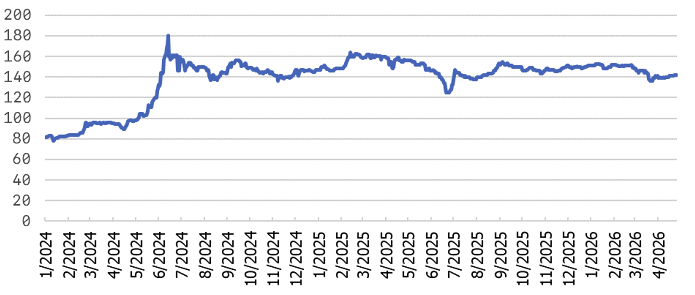

Price Action: Sideways but Supported

Pepper prices have been trading in a narrow band, reflecting a market caught between post-correction consolidation and persistent supply tightness. The absence of sharp directional moves does not signal weakness — rather, it reflects a market where sellers are holding firm and buyers are accumulating cautiously. The corrective phase that preceded this consolidation has largely run its course, and the current price floor is being defended by fundamental supply-side constraints rather than speculative positioning.

Current Price Range – 138,000 – 142,000 VND/kg

Pepper price developments in the Central Highlands and Southeast from First 2024 to 25 Apr, 2026 (Unit: VND/kg)

Domestic and global markets are stabilizing within this corridor, with minimal volatility observed across major trading venues. The range has held despite seasonal selling pressure, indicating that underlying demand is absorbing available supply at these levels.

Despite the recent corrective phase, overall price levels remain relatively high by historical standards. The market is not signaling distress — instead, it is digesting prior gains while supply fundamentals continue to tighten in the background. Traders should view this consolidation as a pause rather than a reversal, with the probability of an upward move increasing as the 2026 crop shortfall becomes more apparent in export data.

Structural Headwinds: Why Supply Is Tightening

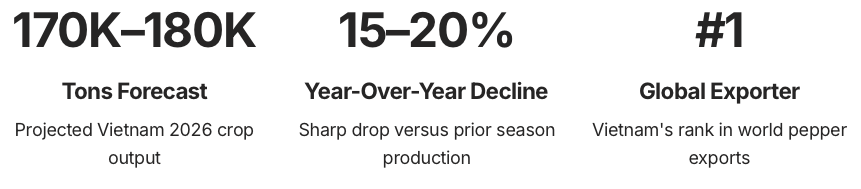

Vietnam’s pepper production for the 2026 crop is forecast at just 170,000 – 180,000 tons, representing a sharp decline of 15% – 20% compared to the prior year. This is not a marginal adjustment — it is a structural contraction that will reverberate through global export supply chains. As the world’s dominant pepper exporter, Vietnam’s output directly sets the tone for global availability and pricing. A shortfall of this magnitude removes a significant volume from the tradable surplus, forcing buyers to compete more aggressively for remaining supply and creating upward pressure on prices that extends well beyond Vietnam’s borders.

Vietnam’s pepper production for the 2026 crop is forecast at just 170,000 – 180,000 tons, representing a sharp decline of 15% – 20% compared to the prior year. This is not a marginal adjustment — it is a structural contraction that will reverberate through global export supply chains. As the world’s dominant pepper exporter, Vietnam’s output directly sets the tone for global availability and pricing. A shortfall of this magnitude removes a significant volume from the tradable surplus, forcing buyers to compete more aggressively for remaining supply and creating upward pressure on prices that extends well beyond Vietnam’s borders.

According to Brazspice Spices, post-harvest selling pressure from Vietnamese farmers is gradually easing. This is a critical signal: when farmers hold back inventory rather than flooding the market, it indicates either price dissatisfaction or genuinely limited available volume. Either way, the direct consequence is a reduction in export supply — exactly the dynamic that supports higher prices over time. The easing of selling pressure also suggests that farmer inventories are thinner than in prior seasons, consistent with the production shortfall forecast for 2026.

Vietnam’s production decline is not the result of a single temporary factor. Three interconnected structural challenges are converging simultaneously, creating a compounding effect on productivity that will be difficult to reverse in the near term. Each challenge on its own would weigh on output; together, they represent a meaningful shift in Vietnam’s ability to supply the global market at prior volumes.

Aging Plantations

A significant portion of Vietnam’s pepper vines are reaching the end of their productive lifecycle. Replanting requires capital investment and a multi-year waiting period before new vines reach full yield, creating a persistent drag on output that cannot be quickly resolved. Many smallholder farmers lack the financial resources to undertake large-scale replanting, meaning this structural constraint will persist across multiple crop cycles and continue to limit Vietnam’s export capacity.

El Niño Weather Stress

Extreme weather patterns linked to El Niño have disrupted growing conditions across Vietnam’s key pepper regions. Irregular rainfall, prolonged heat, and shifting seasonal patterns have reduced yields and increased crop vulnerability, compounding the pressure on already-stressed plantations. The frequency and intensity of these weather events are expected to increase, making yield volatility a persistent risk factor for buyers dependent on Vietnamese supply.

Crop Switching

Faced with volatile pepper prices and rising input costs, many Vietnamese farmers are switching to more profitable alternative crops. This structural migration of acreage away from pepper reduces the total planted area and represents a longer-term supply constraint that extends beyond any single season. Once land is converted to alternatives such as durian, coffee, or fruit trees, the likelihood of returning to pepper cultivation is low, making this acreage loss effectively permanent.

Demand Profile: Stable and Strategic

On the demand side, major consuming markets are showing resilience. The United States, European Union, and China continue to absorb pepper at stable volumes, with a notable shift in buyer behavior: many are moving toward long-term contracts to lock in supply. This trend reflects growing concern about availability and price volatility — buyers are prioritizing supply security over spot-market flexibility, a dynamic that typically supports prices by removing volume from the open market.

🇺🇸 United States

The U.S. remains one of the largest pepper import markets globally, with consistent demand from food manufacturing, foodservice, and retail sectors. American buyers are increasingly favoring forward contracts to mitigate supply risk as global availability tightens.

🇪🇺 European Union

European demand is underpinned by both culinary use and the growing natural ingredients sector. EU buyers are particularly sensitive to quality and traceability, and long-term supplier relationships are becoming more valuable as origin supply becomes less predictable.

🇨🇳 China

China’s domestic consumption and re-export activity continues to provide a stable demand floor. Chinese buyers have been active in securing inventory ahead of anticipated supply tightening, contributing to the supportive price environment.

Contract Shift

Across all three markets, the move toward long-term contracting is reducing the volume of pepper available on the spot market — effectively tightening visible supply and supporting price stability even as physical inventories remain adequate.

Brazil: The Rising Alternative Supplier

As Vietnam’s supply tightens, Brazil is steadily strengthening its position as a reliable alternative origin for global pepper buyers. This is not merely a short-term substitution play — Brazil’s structural advantages in logistics and geographic positioning are making it an increasingly attractive sourcing destination, particularly for Atlantic-facing markets.

Faster Atlantic Routes

Brazil’s Atlantic coastline provides significantly shorter shipping times to U.S. and European ports compared to Southeast Asian origins, reducing lead times and improving supply chain reliability for Western hemisphere buyers.

Lower Logistics Costs

Reduced freight distances translate directly into lower logistics costs, giving Brazilian pepper a competitive edge in delivered pricing — particularly meaningful when global freight rates remain elevated.

Geopolitical Insulation

Brazil’s supply chains are largely insulated from Middle East disruptions that have elevated insurance and freight costs for Asia-Europe routes, providing a risk premium for buyers seeking origin diversification.

Brazil’s controlled and disciplined supply profile — combined with its logistical advantages — means it is well-positioned to capture incremental demand as buyers diversify away from sole reliance on Vietnamese origin. However, Brazil’s production scale remains significantly smaller than Vietnam’s, meaning it can absorb marginal demand shifts but cannot fully offset a structural shortfall from the world’s largest exporter. The combination of controlled Brazilian supply and tight Vietnamese availability creates a market where total global exportable volume is constrained from multiple directions simultaneously.

Market Outlook: Upside Bias Intact

Despite short-term sideways price action, the fundamental setup for pepper markets points toward an upward reversal with high probability. The convergence of tight Vietnamese supply, stable demand from major consuming nations, Brazil’s disciplined export profile, and elevated logistics costs creates a market environment where downside risk is limited and upside potential is significant.

Bullish Factors

- Vietnam 2026 crop down 15–20% year-over-year

- Aging plantations limiting recovery potential

- El Niño weather risks persisting

- Long-term contracting removing spot supply

- Brazil supply controlled and disciplined

Prices are unlikely to decline significantly. The combination of controlled supply from Brazil and tight supply from Vietnam suggests that pepper markets are setting up for a meaningful upward move as 2026 crop realities become fully priced in.