2026 // Week 25 – Vietnam’s Pepper Market: U.S. Imports Hit Record High in April 2026

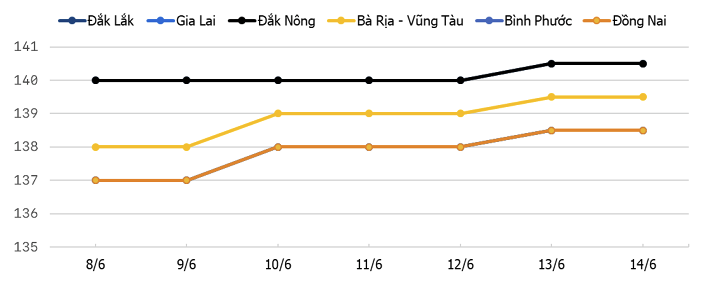

Domestic Market: Prices remain at Elevated Levels

Pepper price trends in the Central Highlands and Southeast regions

during the week of June 08th to June 14th, 2026

Vietnam’s domestic pepper market remained steady, with prices trading between VND 138,000 and 140,000/kg. Although prices are no longer moving sharply higher, the market continues to hold at historically elevated levels.

The key demand-side support is coming from the United States, where importers have significantly increased purchases of Vietnamese pepper while reducing buying from several competing origins.

Stable domestic prices suggest that Vietnam’s market is consolidating after earlier volatility. However, stronger U.S. buying may provide renewed support if export procurement continues into the second half of the year.

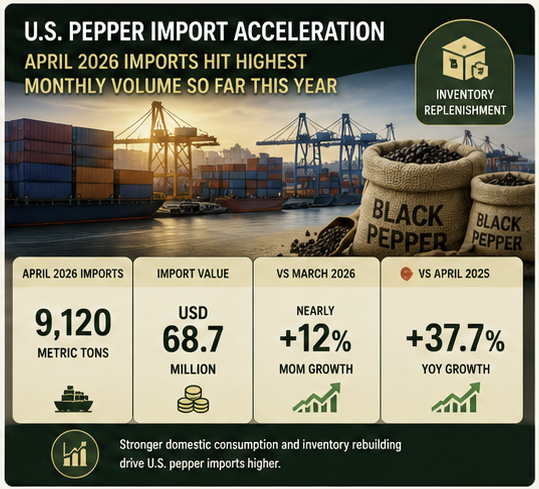

April 2026: A Record-Breaking Month for U.S. Pepper Imports

April 2026 marked a significant milestone in the U.S. pepper import cycle. According to data from the U.S. International Trade Commission, the United States imported 9,120 metric tons of pepper in April, valued at USD 68.7 million — the highest monthly volume recorded so far this year. The month-on-month increase of nearly 12% compared with March, combined with a striking 37.7% year-on-year growth, signals that the U.S. market is accelerating through its demand recovery phase.

The value-to-volume ratio suggests stable pricing conditions, with average import prices holding steady despite the surge in volume. This pattern is consistent with a market transitioning from inventory drawdown to active replenishment — a phase that typically sustains elevated import levels for several consecutive months. For traders monitoring the spice sector, April’s data should be read as a leading indicator of continued strong demand through Q2 and into Q3 2026.

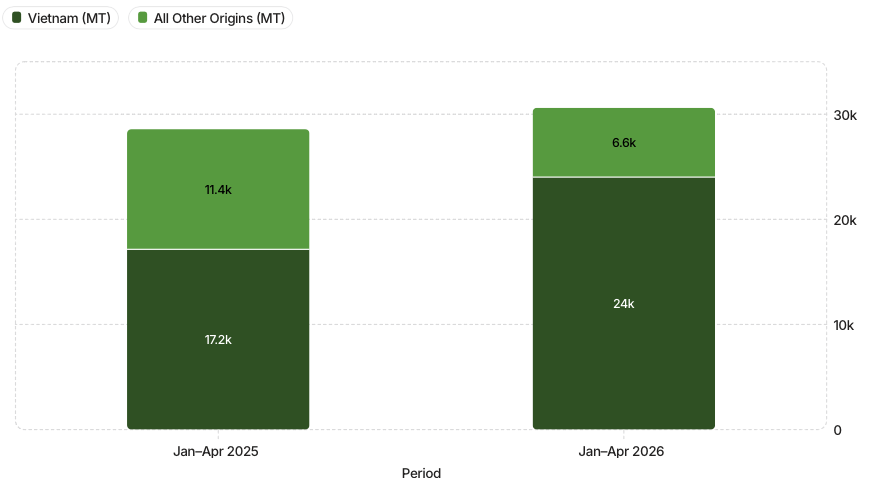

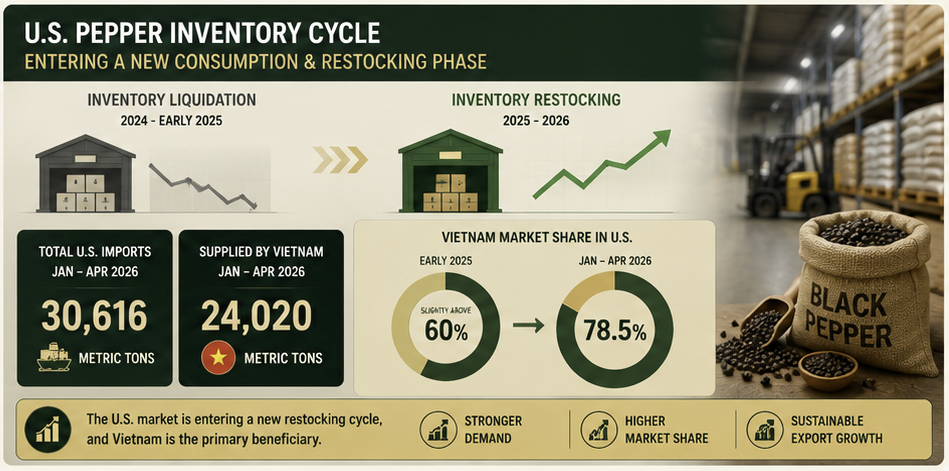

The cumulative picture for the first four months of 2026 further reinforces this trend. Total U.S. pepper imports reached 30,616 metric tons over the January–April period, with Vietnam alone supplying 24,020 metric tons — an increase of nearly 40% compared with the same period last year. This sustained growth trajectory suggests that the April surge is not an isolated event but part of a broader structural shift in U.S. sourcing behavior and consumption patterns.

Vietnam’s Position: 79.4% Market Share in April

Vietnam’s grip on the U.S. pepper market tightened dramatically in April 2026. Vietnamese shipments to the United States reached 7,239 metric tons, representing 79.4% of total U.S. pepper imports for the month. This figure reflects a 20.5% month-on-month increase and a remarkable nearly 75% year-on-year surge — one of the strongest single-country export performances in the spice trade this year.

The cumulative January–April data tells an equally compelling story. Vietnam’s share of the U.S. market climbed from just over 60% in early 2025 to 78.5% through the first four months of 2026. This 18-percentage-point gain in market share represents a fundamental realignment of U.S. sourcing preferences, driven by Vietnam’s competitive pricing, consistent quality, and reliable supply chain performance relative to alternative origins.

The chart above illustrates the dramatic shift in sourcing composition. Vietnam’s cumulative shipments grew by nearly 40% year-on-year, while imports from all other origins contracted sharply over the same period — a clear signal that U.S. buyers are consolidating around Vietnamese supply.

The chart above illustrates the dramatic shift in sourcing composition. Vietnam’s cumulative shipments grew by nearly 40% year-on-year, while imports from all other origins contracted sharply over the same period — a clear signal that U.S. buyers are consolidating around Vietnamese supply.

Competitors Lose Ground: Brazil, Indonesia & China Retreat

As Vietnam surged, competing origins faced steep declines in their U.S. export volumes. The data reveals a broad-based reallocation of U.S. import demand away from traditional alternative suppliers, with Indonesia, China, Brazil, and India all recording significant year-on-year losses in April 2026. This synchronized decline across multiple origins suggests that the shift is driven by structural factors — including relative price competitiveness, quality consistency, and supply reliability — rather than isolated disruptions in any single country.

🇮🇩 Indonesia: -55%

U.S. imports from Indonesia fell by more than 55% in April, the steepest decline among major suppliers. Indonesia’s loss of market share reflects growing price pressure from Vietnamese competition and potential quality consistency concerns among U.S. buyers.

🇨🇳 China: -29%

Chinese pepper shipments to the U.S. declined by nearly 29% year-on-year. Ongoing trade policy uncertainty and shifting buyer preferences toward Southeast Asian origins continue to erode China’s position in the U.S. spice market.

🇧🇷 Brazil: Weakening

Brazilian pepper exports to the United States also weakened in April, though specific percentage data was not disclosed. Brazil has historically served as a secondary supply source for U.S. buyers seeking origin diversification, but that role is diminishing.

🇮🇳 India: Weakening

Indian pepper shipments to the U.S. similarly softened in April. India’s domestic consumption growth and competing export commitments to the Middle East and Europe may be limiting available supply for the U.S. market.

The collective retreat of these four origins underscores a critical market dynamic: U.S. buyers are increasingly prioritizing supply concentration with a single, reliable origin over diversification. Vietnam’s ability to deliver consistent quality at competitive prices, combined with its scale of production, has made it the default choice for American importers seeking to streamline their supply chains. For traders, this trend suggests that non-Vietnamese origins will need to offer meaningful price discounts or differentiated product attributes to regain lost shelf space in the U.S. market.