2026 // Week 23 – Vietnam Black Pepper Exports Surge as U.S. & China Demand Rebounds

Price Stability at Elevated Levels

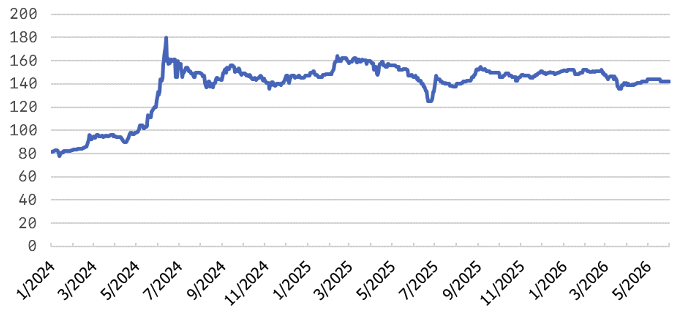

Pepper price developments in the Central Highlands and Southeast from First 2023 to 01-June, 2026 (Unit: VND/kg)

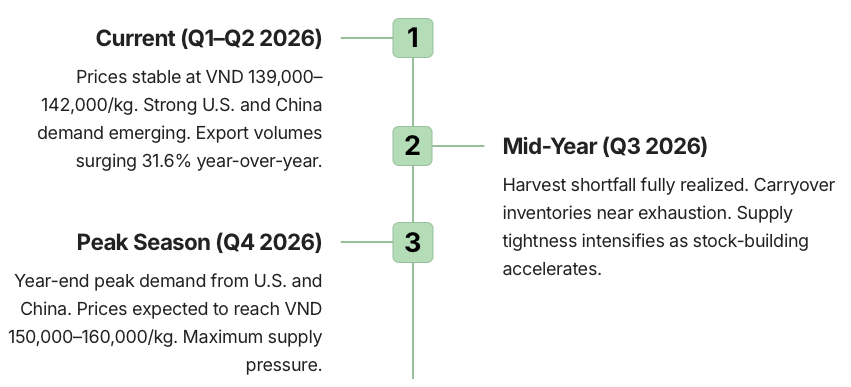

Black pepper prices today are holding firm at VND 139,000–142,000/kg, reflecting strong underlying demand fundamentals despite ongoing supply constraints. Market participants report that buyers are willing to absorb higher prices given the limited availability of quality pepper from major producing regions.

Analysts expect prices to climb further toward VND 150,000–160,000/kg during the peak buying season toward year-end, as carryover inventories have been nearly exhausted and the current harvest season is projected to fall significantly short of prior-year output.

The current price environment reflects a classic supply-demand imbalance, with robust import demand from two of Vietnam’s largest trading partners colliding against a significantly reduced harvest. Buyers who delayed purchases during the cautious purchasing period are now actively competing for available supply, creating upward pressure on domestic prices. Industry observers note that the price stability at these elevated levels — rather than sharp volatility — signals a maturing market where both buyers and sellers are adapting to the new supply reality.

Export Performance: First Four Months

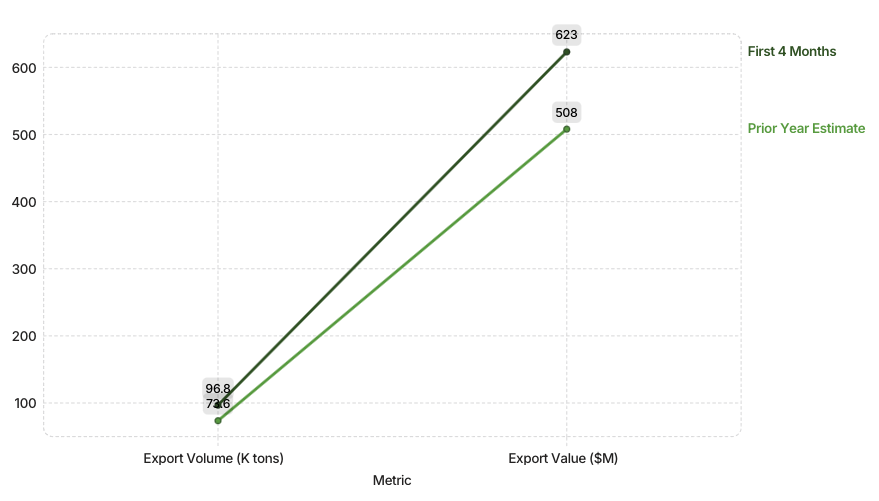

Vietnam’s pepper export sector delivered highly positive results during the first four months of the year, according to the latest agricultural and customs statistics. Total export volume reached 96,800 tons, generating nearly USD 623 million in export revenue. Compared to the same period last year, export volume increased by 31.6%, while export value rose by 22.6% — a clear indication that both volume and pricing are contributing to the sector’s strong performance.

Representatives of the Vietnam Pepper and Spice Association (VPSA) identified the primary driving force behind this growth as the return of international buyers who have actively resumed stockpiling after a prolonged period of cautious purchasing. During the prior year, many importers had adopted a conservative procurement strategy, drawing down existing inventories rather than committing to new purchases amid price uncertainty and global economic headwinds. The shift in buyer behavior reflects growing confidence in demand outlooks, particularly from the U.S. and China, where end-user consumption patterns are recovering and inventory replenishment cycles are accelerating.

The divergence between volume growth (31.6%) and value growth (22.6%) also warrants attention. While both metrics are positive, the fact that volume outpaced value suggests that average export prices per ton were slightly lower than the prior-year baseline, even as absolute prices remain high in domestic terms. This may reflect a shift in product mix — with a greater proportion of standard-grade pepper in the export basket — or the timing of contracts locked in at earlier price points. For agribusiness analysts, this divergence underscores the importance of monitoring both volume and unit-value metrics when assessing the sector’s true revenue performance and margin trajectory.

U.S. Market: Vietnam Consolidates Dominance

Market Share Leadership

In the U.S. market, Vietnam has continued strengthening its leading position, accounting for a commanding 78.1% of import market share. Shipments to the United States reached nearly 25,000 tons during the period, cementing Vietnam’s role as the indispensable supplier for American pepper importers and food manufacturers.

Stock-building activities in the U.S. are expected to continue through the second half of the year, as importers prepare for peak year-end consumption demand. The American market’s reliance on Vietnamese pepper — driven by consistent quality, competitive pricing, and established trade relationships — creates a durable foundation for sustained export volumes.

Stockpiling Cycle

U.S. buyers are actively rebuilding inventories after a prolonged period of conservative purchasing, driving sustained import volumes through H2 2024.

Year-End Peak Demand

Seasonal consumption patterns in the U.S. drive peak demand in Q4, prompting early stock-building by importers and distributors.

Competitive Positioning

Vietnam’s quality consistency and supply reliability have made it the preferred origin for U.S. food service and retail channels.

Looking ahead, the expectation of continued stock-building through the second half of the year suggests that U.S. import volumes could remain elevated well into Q4. This sustained demand, combined with tightening global supply, creates a favorable environment for Vietnamese exporters to negotiate pricing and contract terms.

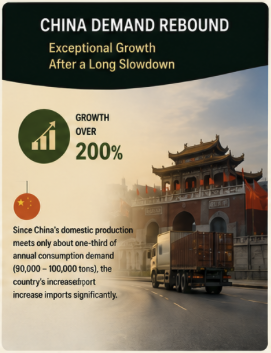

China Market: Exceptional 200%+ Growth After Years of Restraint

China recorded exceptional export growth of more than 200% following a long period of restrained buying, representing one of the most significant demand surprises in the current market cycle. This dramatic rebound underscores the pent-up demand that had accumulated during China’s extended period of conservative procurement, and signals a fundamental shift in Chinese import behavior that could have lasting implications for Vietnam’s export strategy.

China recorded exceptional export growth of more than 200% following a long period of restrained buying, representing one of the most significant demand surprises in the current market cycle. This dramatic rebound underscores the pent-up demand that had accumulated during China’s extended period of conservative procurement, and signals a fundamental shift in Chinese import behavior that could have lasting implications for Vietnam’s export strategy.

China’s Consumption Gap

China’s domestic production capacity satisfies only roughly one-third of its annual consumption demand, which is estimated at 90,000–100,000 tons per year. This structural supply deficit compels China to increase imports significantly, creating a durable and growing market for Vietnamese pepper exporters.

Import Dependency Rising

With domestic output unable to close the gap between production and consumption, China is increasingly reliant on foreign supply. Vietnam, as the world’s largest pepper exporter, is the natural beneficiary of this structural import demand, particularly given geographic proximity and established trade corridors.

Rebound Drivers

The surge in Chinese imports follows years of restrained purchasing, suggesting that inventory drawdowns have reached critical levels. Chinese buyers are now actively replenishing stocks, and the recovery in domestic economic activity is supporting stronger end-user demand across food service and manufacturing channels.

The structural nature of China’s import demand is particularly significant for long-term market planning. Unlike cyclical demand fluctuations that reverse within a single season, China’s consumption gap is rooted in fundamental agricultural and demographic factors that are unlikely to change in the near term. Domestic production capacity is constrained by land-use competition, labor availability, and the relative economics of pepper cultivation versus alternative crops — all of which suggest that China’s import dependency will persist and potentially deepen over time.

Supply Constraints: Harvest Decline & Inventory Drawdown

Alongside the positive export outlook, supply shortages are becoming increasingly evident and are emerging as a critical factor shaping the market. Total harvest output this season is estimated to decline by 15%–20%, falling to approximately 170,000–180,000 tons, due to a combination of unfavorable weather conditions and farmers shifting to alternative crops. In addition, carryover inventories from last year have been nearly exhausted, removing a key buffer that had previously helped stabilize supply during demand spikes.

Weather-related yield reductions have been particularly pronounced in the Central Highlands and Southeast regions, which together account for the majority of Vietnam’s pepper production. Prolonged dry spells followed by irregular rainfall patterns disrupted flowering and fruiting cycles, directly impacting both volume and quality of the harvest.

Unfavorable Weather

Irregular rainfall and temperature fluctuations reduced yields across major growing regions, particularly in the Central Highlands where the majority of Vietnam’s pepper is cultivated.

Crop Substitution

Farmers are increasingly shifting to alternative crops — including durian, coffee, and rubber — that offer more attractive economic returns, permanently reducing pepper cultivation area.

Exhausted Carryover Stocks

Inventories held over from the previous season have been nearly depleted, removing a critical supply buffer and amplifying the impact of the current harvest shortfall on market prices.

The convergence of these supply-side pressures creates a fundamentally tighter market environment that is likely to persist through the remainder of the year. With carryover inventories depleted and the current harvest falling short, the available supply pool is significantly constrained at precisely the moment when import demand is accelerating. This dynamic is the primary support factor keeping domestic prices elevated and underpins analyst expectations for further price appreciation toward year-end.

Price Outlook: Toward VND 150,000–160,000/kg by Year-End

Tight supply has become a strong support factor keeping domestic pepper prices elevated, with some experts expecting prices to move toward VND 150,000–160,000/kg during the peak buying season toward year-end. This projected price trajectory reflects the compounding effect of multiple bullish factors converging simultaneously: surging import demand, a significantly reduced harvest, depleted carryover stocks, and seasonal stock-building activity that typically accelerates in the second half of the year.

Operational Risks: Regulatory & Logistics Headwinds

Beyond supply-demand pressures, the pepper industry is navigating a complex array of regulatory and logistical challenges that are adding cost and complexity to export operations. Newly implemented regulations governing the registration management of foreign exporting enterprises now require procedures, packaging, and food safety systems to be standardized to the highest degree. At the same time, geopolitical tensions in the Middle East are increasing ocean freight costs and disrupting logistics networks, directly affecting shipment and delivery schedules.

Ongoing geopolitical tensions in the Middle East are having a direct and measurable impact on pepper export logistics. The disruption to Red Sea shipping routes has forced vessels to take longer alternative routes around the Cape of Good Hope, adding 10–14 days to transit times and significantly increasing ocean freight costs.

Freight Cost Increases: Ocean freight rates have risen substantially, adding direct cost pressure to export margins and making price competitiveness more challenging.

Delivery Schedule Disruption: Extended transit times and port congestion are disrupting shipment schedules, requiring exporters to build larger safety buffers into delivery commitments.

Insurance & Risk Premiums: Elevated geopolitical risk is driving up cargo insurance costs, further compressing net export returns for Vietnamese suppliers.

These regulatory and logistical challenges are not temporary disruptions but rather structural shifts that require sustained investment and adaptation. Companies that proactively upgrade their compliance infrastructure and diversify their logistics partnerships will be better positioned to navigate this environment than those that react only when problems arise. The regulatory burden, while costly in the short term, may ultimately serve as a barrier to entry that benefits established, well-capitalized exporters by limiting competition from smaller, less-compliant operators.

Industry Direction: Integration, Certification & Value-Added Processing

To overcome mounting challenges, the Vietnamese pepper industry is shifting strongly toward supply-chain integration and sustainable farming practices. Experience from key growing regions demonstrates that products holding organic certification are consistently purchased at premiums ranging from 10%–30% above open market prices — a significant margin enhancement that rewards producers who invest in certification and quality systems.

Organic Certification Premium

Certified organic pepper commands 10%–30% premiums over conventional product. Leading growing regions are investing in certification programs to capture this value differential and access premium market segments in Europe and North America.

Deep-Processing Investment

Leading enterprises are actively investing in deep-processing technologies — including extraction, grinding, and value-added product formats — to enhance product value and reduce dependence on raw commodity exports. This shift improves margins and diversifies revenue streams.

Niche Market Expansion

Alongside quality improvement, exporters are actively expanding into niche markets — including organic, fair-trade, and single-origin segments — that offer higher margins and more loyal customer bases than commodity-grade pepper markets.