2026 // Week 29 – Vietnam Pepper Market Update: Prices Firm at Record-High Levels

Domestic Market

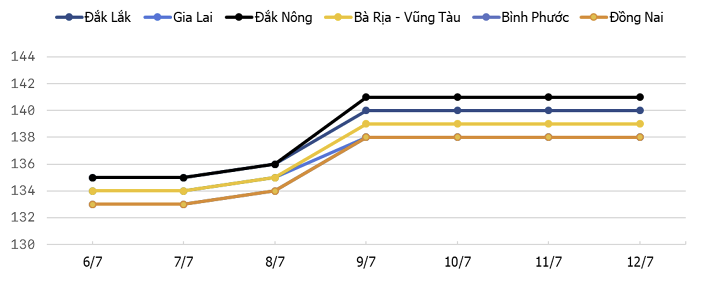

Pepper price trends in the Central Highlands and Southeast regions

during the week of July 06th to July 12th, 2026

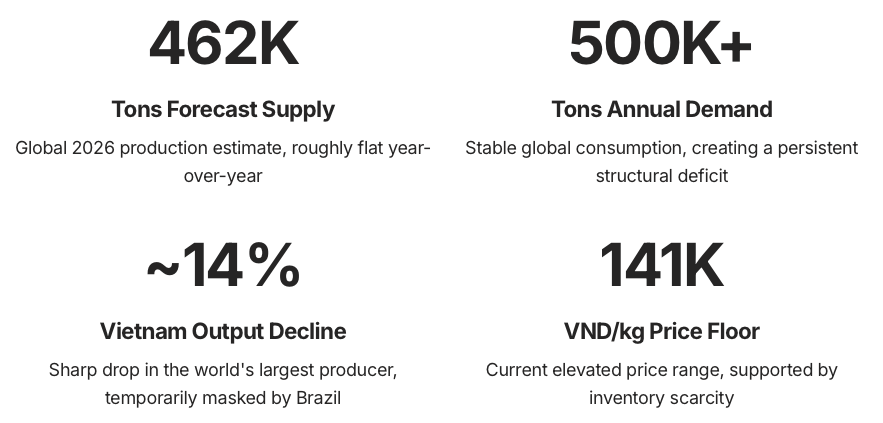

Global black pepper prices held stable today at 138,000–141,000 VND/kg — elevated levels reflecting a market under severe structural strain. The stability masks a deeper reality: global inventories have been drawn down to a record low, with consumption consistently outpacing production since 2021. A Holland-based commodity assessor confirms that continuous deficits have eroded reserves to below annual global consumption — a precarious position for any soft commodity market.

Despite mild short-term fluctuation, the long-term trend remains strongly supported by widespread supply scarcity. The combination of rock-bottom inventories, aging plantation infrastructure, and looming weather disruption creates a supply environment with limited near-term relief.

The Inventory Crisis: A Structural Supply Deficit

The most critical dynamic in today’s pepper market is the collapse of global inventories. Per the latest assessment from a Holland-based commodity analyst, a continuous production deficit since 2021 has severely eroded global reserves. Inventories have now fallen below annual global consumption — meaning the world effectively has less pepper in storage than it consumes in a single year. This is an extraordinary position for a commodity that historically maintained comfortable buffer stocks.

Global demand remains stable and robust at above 500,000 tons per year, while 2026 supply is forecast at approximately 462,000 tons — roughly flat versus the prior year. That leaves a structural gap of nearly 40,000 tons that must be filled from dwindling reserves. With those reserves already critically depleted, there is no meaningful buffer left to absorb further supply shocks.

The deficit is not a temporary anomaly — it is the result of multi-year underproduction compounding against steady demand growth. Each season that production fails to meet consumption draws further on reserves that are already critically low. For market participants, this inventory picture represents the single most important bullish factor supporting prices at current elevated levels and beyond.

Vietnam & Indonesia: Production Under Pressure

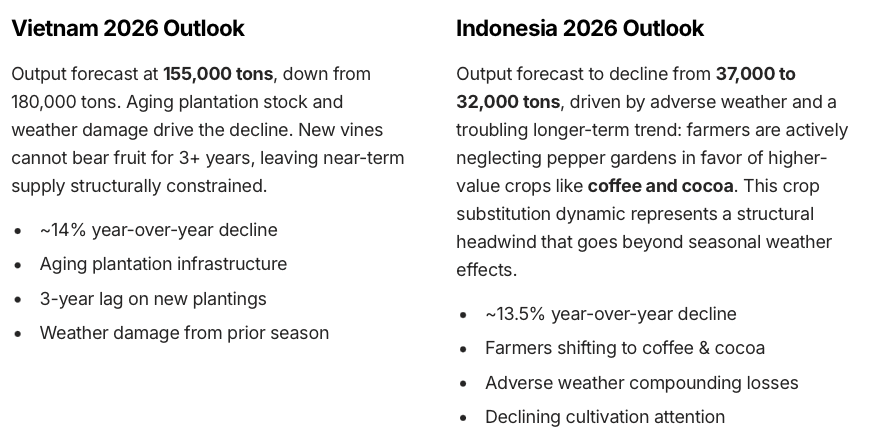

Vietnam, the world’s dominant pepper producer, faces a sharp contraction in 2026 output. Supply is estimated to fall to just 155,000 tons, down from 180,000 tons in the prior season — a decline of approximately 14%. This drop is driven by a combination of adverse weather impacts from the prior growing season and a structural problem that cannot be quickly resolved: a high proportion of aging plantations that are increasingly unproductive.

While new planting has begun in some Vietnamese localities, near-term shortage pressure remains fundamentally unresolved. New pepper vines require a minimum of 3 years to bear fruit, meaning any planting activity undertaken today will not contribute to supply until at least 2028–2029. The lag between investment and output creates a dangerous gap in the supply timeline that no amount of current planting activity can close in the near term.

Brazil: The Sole Bright Spot — But With Limits

Amid widespread production declines across the major growing regions, Brazil stands out as the only significant positive story in the 2026 pepper supply picture. Output is expected to reach 118,000 tons, representing approximately 7% growth versus the prior year. This expansion is driven by technical improvements in cultivation practices and a meaningful increase in planted area — a rare combination of yield and acreage growth in an otherwise contracting global supply environment.

Brazil’s growth has been critical in temporarily offsetting the sharp ~14% decline from Vietnam. Without Brazil’s contribution, the global supply picture would be considerably more dire. However, it is important for market participants to understand that Brazil’s growth, while welcome, is insufficient to close the overall supply-demand gap — and even Brazil faces its own structural constraints that may limit future expansion.

Technical Improvements Driving Growth

Brazil’s pepper sector has benefited from meaningful investment in cultivation technology and farm management practices. Improved irrigation, better varietal selection, and more professional agronomic management have contributed to both yield gains and area expansion. These improvements position Brazil as the most dynamic pepper-producing region in the current cycle.

Coffee Competition Constrains Upside

Despite the positive outlook, Brazil’s pepper sector faces a significant headwind: competition from coffee. Coffee cultivation in Brazil benefits from substantially greater mechanization advantages, making it more economically attractive for large-scale operators. This shift in crop priority means that even Brazil’s growth potential has a ceiling — land and capital that might otherwise expand pepper production are flowing toward coffee instead.

The net result is a global supply picture where Brazil’s +7% growth is mathematically overwhelmed by Vietnam’s −14% and Indonesia’s −13.5% declines. Brazil’s contribution, while positive, is best understood as mitigating the severity of the deficit rather than resolving it. The overall supply-demand imbalance remains severe, and Brazil alone cannot fill the gap left by contracting output across Asia.

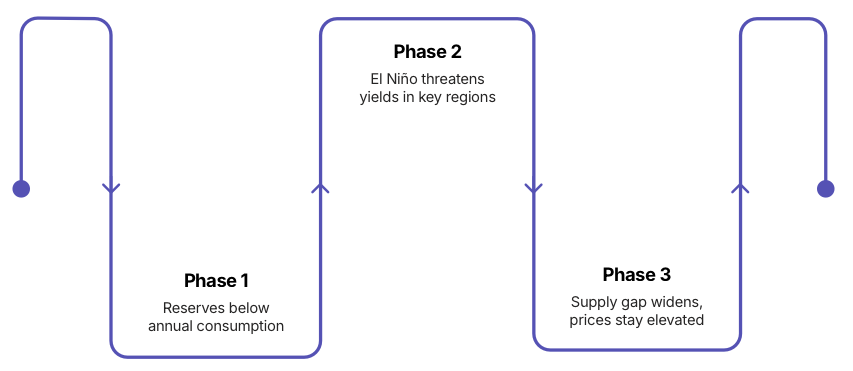

El Niño Threat & Long-Term Price Outlook

The supply tension described above is expected to escalate further as meteorological forecasts point to a strong El Niño event returning late this year. El Niño weather patterns are historically disruptive to pepper yields across all key growing regions — Vietnam, Brazil, India, and Indonesia. The timing is particularly concerning given that inventories are already at record lows, leaving the market with virtually no buffer to absorb additional production losses.

For traders and supply-chain managers, the market is gradually shifting its focus from annual production figures to available inventories.

Several years of global production deficits have significantly reduced carry-over stocks, making the market increasingly sensitive to weather developments and any disruption to export-quality supply.

While Brazil is expanding production, reduced output from Vietnam and Indonesia continues to limit the overall increase in global availability.

At current levels, downside appears limited unless export demand weakens materially.

This Week’s Focus

- Brazil export pace.

- Indonesia harvest progress.

- El Niño developments.

- China buying activity.

- SPS implementation across key importing markets.