2026 // Week 26 – Vietnam Pepper Market: June 2026 Mid-Month Report

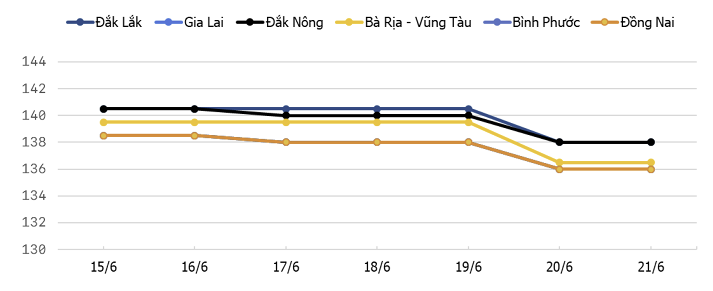

Domestic Prices Under Pressure

Pepper price trends in the Central Highlands and Southeast regions

during the week of June 15th to June 21th, 2026

Vietnam’s domestic pepper prices experienced a sharp correction during the first half of June, declining by as much as VND 3,000 per kilogram. Prices are currently trading in the range of VND 137,000 to VND 140,000 per kilogram — a meaningful pullback from recent highs that has drawn attention from both domestic growers and international buyers monitoring sourcing costs.

The price decline reflects typical seasonal dynamics as the main harvest period progresses and supply availability increases in key growing regions such as Dak Lak, Ba Ria-Vung Tau, and Gia Lai. Traders and processors have been actively building inventory ahead of the peak export window, which has contributed to downward pressure on farmgate prices. The VND 3,000/kg drop, while notable in percentage terms, should be viewed within the context of the broader price cycle — domestic pepper prices had rallied significantly in preceding months, making this correction a partial normalization rather than a structural break.

Export Surge: Volume & Value Up ~20%

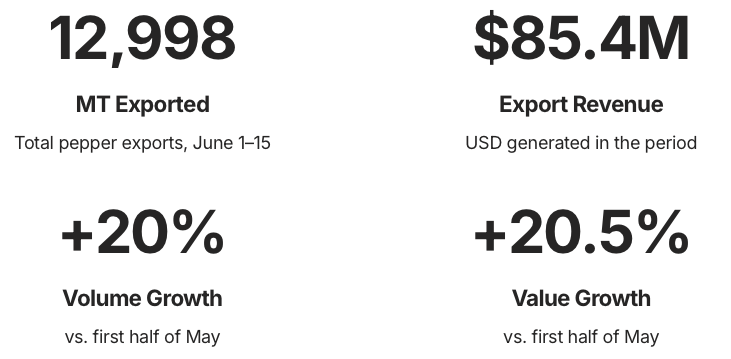

While domestic prices softened, Vietnam’s pepper export performance in the first half of June was outstanding. According to data from the Vietnam Pepper and Spice Association (VPSA), the country exported 12,998 metric tons of pepper during the first 15 days of June, generating export revenue of USD 85.4 million.

Compared with the first half of May, exports increased by 20% in volume and 20.5% in value — a near-parallel surge that indicates unit prices at the export level remained relatively stable despite domestic price weakness. This divergence between domestic and export pricing underscores the premium that international buyers are willing to pay for Vietnamese pepper, particularly as global supply from other origins tightens.

VPSA member companies were the primary drivers of this export surge, accounting for 11,293 MT — nearly 87% of total exports — and posting a remarkable 34.6% increase compared with the previous period. The outsized growth among VPSA members relative to the overall market suggests that larger, organized exporters are capturing a growing share of international demand, potentially at the expense of smaller, non-member traders who may face tighter financing or logistics constraints.

The strong export performance also reflects favorable conditions in destination markets. Asian buyers, in particular, have been actively restocking amid concerns about supply availability from other origins later in the year. European and Middle Eastern demand has remained resilient, supported by steady foodservice recovery and sustained retail demand for spice products. The near-identical growth rates in volume and value (20% vs. 20.5%) further indicate that the export mix remained stable, with no significant shift toward lower-value pepper categories that might have diluted average unit prices.

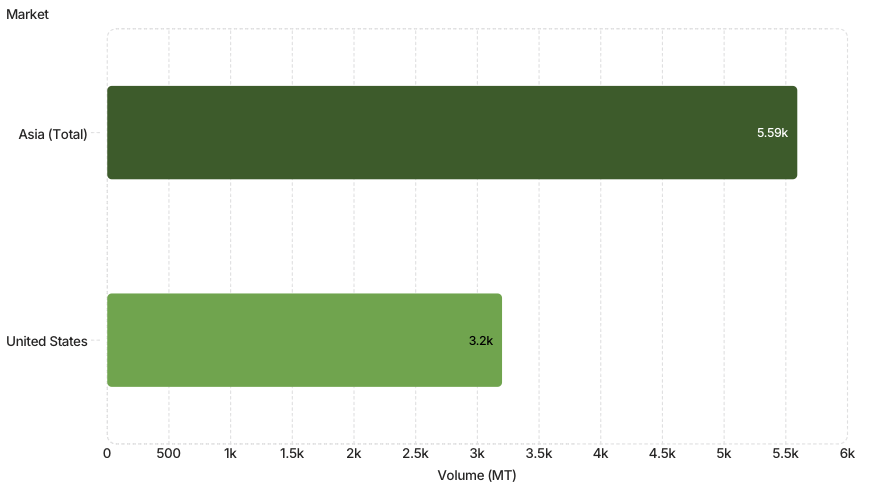

Destination Markets: Asia Leads, US Tops Single Markets

Asia maintained its position as Vietnam’s largest pepper export destination during the first half of June, absorbing 5,593 MT — equivalent to 43% of total exports. The region’s dominant share reflects sustained demand from traditional buyers in China, Japan, and Southeast Asia, where Vietnamese pepper remains a preferred sourcing option due to its quality consistency and competitive pricing.

The United States retained its status as Vietnam’s largest single-country market, importing 3,200 MT during the period. US demand for Vietnamese pepper has been underpinned by strong retail and foodservice consumption, as well as ongoing inventory replenishment by major spice blenders and food manufacturers. The UAE, Germany, and India followed as the next most significant destinations, each representing important regional gateways — the UAE for Middle Eastern and North African redistribution, Germany for broader European distribution, and India for both domestic consumption and re-export activity.

The chart above highlights the two largest destination categories by volume. Asia’s aggregate 5,593 MT dwarfs any single-country destination, while the United States at 3,200 MT stands as the clear leader among individual markets. The remaining volume — approximately 4,205 MT — was distributed across the UAE, Germany, India, and other smaller destinations not broken out in the VPSA data.

From a strategic perspective, the geographic concentration of exports presents both opportunities and risks for Vietnamese exporters. The heavy reliance on Asia (43%) and the US (approximately 25% of total exports) means that demand disruptions in either region could significantly impact overall export volumes. However, the diversity within Asia — spanning multiple countries with varying demand cycles — provides some natural hedging. The continued presence of European buyers (Germany) and emerging market demand (India, UAE) also offers diversification potential that exporters are actively developing.

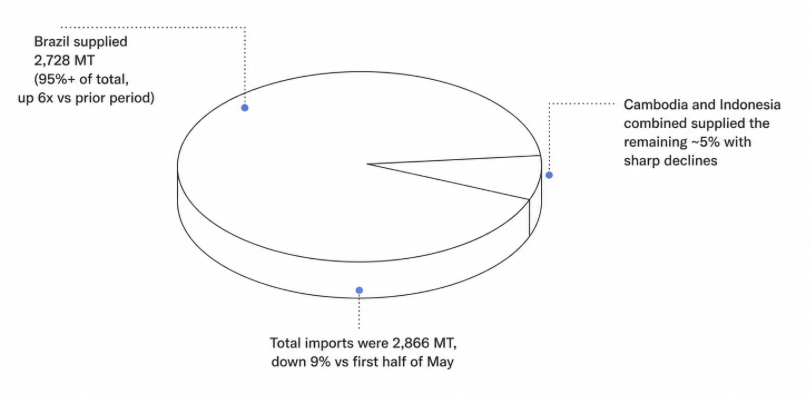

Import Dynamics: Brazil Dominates Supply

On the import side, Vietnam brought in 2,866 MT of pepper during the first half of June, representing a 9% declinecompared with the first half of May. This reduction in import volumes is consistent with seasonal patterns, as domestic supply from the main harvest typically reduces the need for supplementary imports during the June–July period.

The most striking feature of June’s import data is Brazil’s overwhelming dominance. Brazil supplied 2,728 MT, accounting for more than 95% of Vietnam’s total pepper imports — and representing a more than sixfold increasecompared with the previous period. This dramatic surge in Brazilian supply reflects both competitive pricing from Brazilian origins and Vietnam’s role as a processing and re-export hub, where lower-cost Brazilian pepper is blended or repackaged before being shipped to international markets.

Meanwhile, imports from Cambodia and Indonesia — historically significant supplementary supply sources for Vietnam — declined sharply during the period. The contraction from these origins likely reflects reduced availability as their own harvest seasons wind down, as well as potentially less competitive pricing relative to Brazilian pepper. The shift toward Brazilian supply also suggests that Vietnamese importers are prioritizing cost efficiency, taking advantage of Brazil’s large harvest volumes and favorable exchange rate dynamics.