11 May 2026

11 May 20262026 // Week 20 – Vietnam Pepper Market: Domestic Prices Anchored at Historic Highs

Domestic Price Landscape: Stability at Elevated Levels

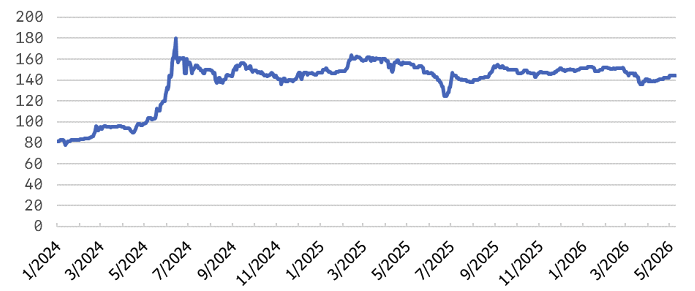

Pepper prices within Vietnam’s domestic market have stabilized in a tight band of VND 140,000–144,000/kg, representing the upper end of the historical price range. This stability reflects a market in careful equilibrium — strong enough to reward producers handsomely, yet not so overheated as to trigger speculative frenzy. The price floor has held consistently, suggesting genuine structural support rather than temporary volatility.

Pepper price developments in the Central Highlands and Southeast from First 2023 to 09-May, 2026 (Unit: VND/kg)

Behind this stability lies a complex set of behavioral dynamics. Many farmers and local traders are deliberately withholding inventory from the market, betting that prices will climb further in the coming months. This inventory-holding behavior, while rational at the individual level, creates a self-reinforcing cycle: reduced available supply keeps prices elevated, which in turn encourages more holding. The result is a market where reported prices are high, but actual transaction volumes at those prices may be thinner than they appear.

Market Sentiment: Cautiously Optimistic

Despite record-high prices, traders and farmers are not rushing to sell. Inventory accumulation strategies are widespread, with market participants anticipating further price appreciation driven by supply constraints and sustained export demand.

Global demand, while solid, has not yet delivered the breakout momentum that would justify an immediate price surge beyond current levels. International buyers are absorbing supply at a steady pace, but there is no evidence of panic-buying or contract-rushing behavior that typically accompanies true supply crises. This measured demand profile helps explain why prices have stabilized rather than continued climbing — the market is balancing strong fundamentals against realistic demand expectations.

Import Surge: Vietnam’s Aggressive Procurement Strategy

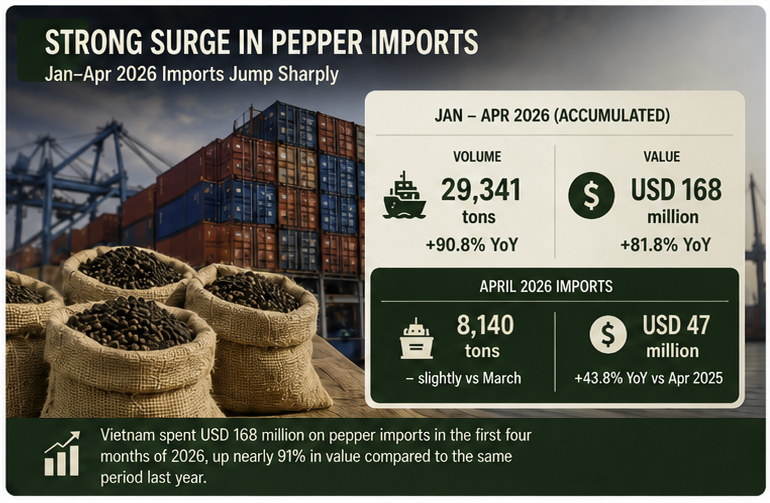

The most striking development in Vietnam’s pepper market in early 2026 is the dramatic acceleration of raw material imports. In April alone, Vietnam imported more than 8,140 tons of pepper valued at USD 47 million. While this represented a slight month-on-month decline from March’s peak, the year-on-year comparison tells a far more dramatic story: April 2026 import volumes were up 43.1% compared to April 2025, with black pepper accounting for the overwhelming majority of shipments.

Cumulatively, the first four months of 2026 saw Vietnam import 29,341 tons of pepper across all varieties, at a total cost of approximately USD 168 million. This represents a 90.8% increase in volume and an 81.8% increase in import value compared to the same period in 2025 — a near-doubling of procurement activity that underscores the urgency of Vietnam’s supply situation. The scale of this increase is difficult to overstate: it represents a fundamental shift in how Vietnam sources pepper, moving from a predominantly self-sufficient producer to an active and growing importer.

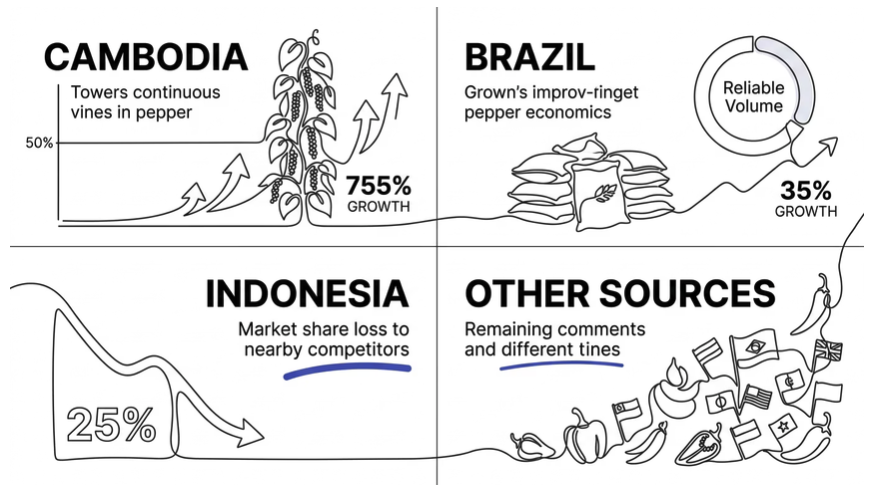

Supply Origins: Cambodia Dominates, Brazil Grows, Indonesia Fades

Vietnam’s import portfolio in early 2026 reveals a significant geographic realignment in pepper sourcing. Cambodia has emerged as Vietnam’s most critical supplier by a wide margin, with exports to Vietnam surging by an extraordinary 755% year-on-year. Cambodian pepper now accounts for more than 50% of Vietnam’s total pepper imports — a dominant position that reflects both geographic proximity and Cambodia’s expanding pepper cultivation capacity.

Brazil, traditionally a major player in the global pepper market, has also increased its shipments to Vietnam by 35%, reinforcing its position as a reliable secondary supplier. In contrast, Indonesia — historically one of the world’s leading pepper exporters — has seen its supply to Vietnam decline, reflecting either domestic supply constraints, competitive pricing challenges, or shifting export priorities toward other markets. This divergence between Brazil’s growth and Indonesia’s decline highlights the competitive dynamics reshaping Southeast Asia’s pepper trade flows.

Strategic Outlook: What the Data Signals

The convergence of elevated domestic prices, aggressive import procurement, and shifting supply geography points to a Vietnam pepper market undergoing structural transformation. The data from early 2026 is not merely a snapshot of short-term volatility — it reflects deeper trends in production capacity, supply chain strategy, and Vietnam’s evolving role in the global spice trade.

Analysts view the aggressive procurement of pepper from external sources as a strategic move aimed at compensating for domestic supply shortages. This helps maintain stability in supply chains for deep processing activities and fulfillment of international export contracts as domestic production is no longer as abundant as in previous years.