2026 // Week 15 – Global Pepper Market: Price Stability and Supply Forecasts

Global Pepper Market Update

Domestic Vietnamese pepper prices held firm today at 139,000 – 141,000 VND/kg, reflecting a week of stable trading with covering demand emerging across the market. While Vietnam’s domestic picture remains steady, international pepper markets are experiencing notable price movements — with Indonesia and Brazil both recording upward trends in recent days. The divergence between stable Asian origins and rising prices in Latin America and Southeast Asia underscores the growing complexity of the global pepper trade environment.

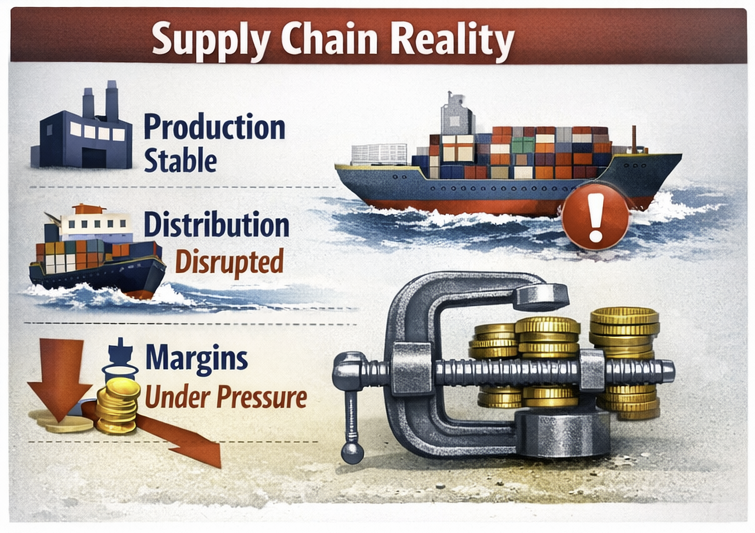

At the same time, geopolitical developments in the Middle East are beginning to ripple through global supply chains in ways that extend well beyond the conflict zone itself. Brazilian pepper exporters — particularly those in Espírito Santo — are among the first to feel the indirect effects, as shipping route disruptions, surging cargo insurance premiums, and rising logistics costs begin to erode the competitiveness of one of the world’s most important pepper-producing regions. The situation is a stark reminder that in today’s interconnected trade environment, events thousands of kilometers from a production zone can have direct and measurable consequences for exporters, cooperatives, and farmers alike.

Pepper price developments in the Central Highlands and Southeast from First 2023 to 06-April, 2026 (Unit: VND/kg)

Price Movements Across Key Origins

Today’s trading session saw Vietnam’s domestic pepper prices hold steady in the 139,000 – 141,000 VND/kg range, a level that has persisted throughout the week. The stability reflects a balance between modest covering demand from buyers and a generally cautious tone among sellers who are not yet under pressure to move volume aggressively. Vietnamese pepper has maintained its position as a reliable and competitively priced origin, continuing to attract consistent interest from both regional and international buyers.

Beyond Vietnam, the picture is more dynamic. Pepper prices in both Indonesia and Brazil have recorded an upward trend over the same period, driven by a combination of tightening supply availability and growing cost pressures on the export side. In Indonesia, domestic supply constraints and firm export demand have supported higher price levels, while in Brazil, the upward movement is increasingly tied to the logistics and shipping cost pressures emerging from the broader geopolitical environment. These divergent price signals across origins are worth watching closely, as they may begin to influence buyer sourcing decisions and contract negotiations in the coming weeks.

Geopolitical Tensions Reshape Shipping Routes

The conflict involving the United States and Iran, while geographically distant from pepper-producing regions, is already exerting a measurable impact on global trade flows. According to Rural Total, black pepper produced in Espírito Santo — one of Brazil’s key agricultural products — is facing a more complex operating environment as a direct consequence of these geopolitical tensions. The effects are not on production itself, but on the distribution channels and logistics infrastructure that connect Brazilian farms to international buyers.

As tensions escalate, major shipping lines are adjusting routes to avoid high-risk areas, resulting in longer transit times and significantly higher transportation costs. For pepper exporters, these route adjustments translate directly into reduced competitiveness against other producing countries that are not exposed to the same logistical headwinds. The impact is particularly acute for Espírito Santo, which maintains long-established trade relationships with Persian Gulf markets— countries that account for approximately 16% of the state’s pepper exports. This concentration in a geopolitically sensitive region creates a structural vulnerability that is difficult to address in the short term

Espírito Santo: A Critical Node Under Pressure

Espírito Santo occupies a central position in Brazil’s pepper export landscape, producing black pepper that is widely recognized for its quality and consistency. The state’s export profile is heavily weighted toward strategic markets in the Persian Gulf region, a trade relationship built over decades and representing approximately 16% of total pepper export volume. While this concentration has historically been a source of strength — providing reliable demand from well-established trading partners — it has also created a structural exposure that is now being tested by the current geopolitical environment.

The challenge is not simply one of cost. Market concentration limits the ability to redirect shipments quickly when disruptions occur. A significant portion of Espírito Santo’s pepper exports flows toward regions currently facing instability, and building alternative market relationships takes time, investment, and often a willingness to accept different pricing dynamics. In the short term, exporters have limited flexibility to shift volumes away from affected destinations without incurring additional costs or accepting lower returns.

Key Supply Chain Stakeholder

Cooabriel and other key cooperatives in the region are closely monitoring the situation. While no direct impact on production volumes has been recorded to date, the indirect effects of global instability are already being felt — particularly in the logistics segment, which remains one of the most sensitive variables in international agricultural trade. Cooperatives are working with exporters to evaluate alternative routing options and assess the feasibility of diversifying destination markets over the medium term.

Farmers, cooperatives, and exporters are jointly tracking international developments and evaluating strategic adjustments designed to mitigate risk and preserve Brazil’s presence in the global pepper market. These efforts include exploring alternative shipping corridors, engaging with buyers in less exposed markets, and building greater flexibility into contract structures to accommodate the current volatility in logistics costs.

Risk Concentration Factors

- ~16% of Espírito Santo pepper exports directed to Persian Gulf markets

- Limited short-term ability to redirect shipments to alternative destinations

- Logistics costs now a primary driver of export competitiveness

- Insurance premiums nearly doubled for high-risk routing zones

- Market concentration amplifies exposure to single-region disruptions

The situation in Espírito Santo illustrates a broader lesson for agricultural commodity exporters: market diversification is not merely a strategic preference but a risk-management imperative. Dependence on a limited number of destination markets increases trade risk, especially in a volatile global environment where external geopolitical factors can disrupt trade flows with little warning.